Availability of Credit In Special Cases Under GST

CA. Ankush R Paliwal

Under GST, a registered person is entitled to take credit of input tax charged on the supply of goods or services or both supplied to him which are used or intended to be used in the course or furtherance of his business. But there are certain cases where credit in respect of inputs and capital goods received before getting registered can be claimed or where credit can be transferred by one registered person to another registered person. This article lists out such cases and the procedure to be followed for the same.

Section 18 of the CGST Act, 2017 lists out the situations where credit can be claimed in special cases which are as under:

Registered Person Becomes Liable For Registration (Section 18(1)(a)):

Where a person liable for registration applies for registration within 30 days of becoming liable and has been granted registration shall be entitled to take credit of input tax in respect of inputs held in stocks and inputs contained in semi-finished goods or finished goods held in stock on the day immediately preceding the date from which he becomes liable to pay tax under the provisions of this Act.

Voluntary Registration (Section 18(1)(b)):

Where a person is not required to take registration but takes voluntary registration under Section 25(3) then he shall be entitled to take credit of input tax in respect of inputs held in stocks and inputs contained in semi-finished goods or finished goods held in stock on the day immediately preceding the date of grant of registration.

Opting from Composition Scheme to Regular (Section 18(1)(c)):

Where any registered person ceases to pay tax under section 10, he shall be entitled to take credit of input tax in respect of inputs held in stocks and inputs contained in semi-finished goods or finished goods held in stock and on capital goods on the day immediately preceding the date from which he becomes liable to pay tax under section 9, provided that the credit on capital goods shall be reduced by such percentage points as may be prescribed.

When Exempt Supply becomes Taxable Supply( Section 18(1)(d)):

Where an exempt supply of goods or services or both by a registered person becomes a taxable supply then such person shall be entitled to take credit of input tax in respect of inputs held in stocks and inputs contained in semi-finished goods or finished goods held in stock relatable to such exempt supply and on capital goods exclusively used for such exempt supply on the day immediately preceding the date from which such supply becomes taxable, provided that the credit on capital goods shall be reduced by such percentage points as may be prescribed.

Change in Constitution of Registered Person( Section 18(3)):

Where there is a change in the constitution of a registered person on account of the sale, merger, demerger, amalgamation, lease, or transfer of the business with the specific provisions for transfer of liabilities, the said registered person shall be allowed to transfer the input tax credit which remains unutilized in his electronic credit ledger to such sold, merged, demerged, amalgamated, leased or transferred business in such manner as may be prescribed. It is clarified that transfer or change in the ownership of the business will include transfer or change in the ownership of business due to the death of the sole proprietor. In case of death of sole proprietor if the business is continued by any person being transferee or successor, the input tax credit which remains

un-utilized in the electronic credit ledger is allowed to be transferred to the transferee.

Procedure to Claim Credit as per CGST Rules, 2017:-

(A) In Case 1 to 4 Above:

As per Rule 40(1)(b) & 40(1)(c), the registered person shall make a declaration within 30 days from the date of becoming eligible to avail the input tax credit as mentioned above in Form ITC-01 specifying the details of the inputs held in stock or inputs contained in semi-finished goods or finished goods held in stock or as the case may be, capital goods:

a) On the day immediately preceding the date from which he becomes liable to pay tax under the provisions of the Act in case of a claim under section 18(1)(a).

b) On the day immediately preceding the date of grant of registration in case of a claim under section 18(1)(b).

c) On the day immediately preceding the date from which he becomes liable to pay tax under section 9, in case of a claim under section 18(1)(c).

d) On the day immediately preceding the date from which the supplies made by the registered person becomes taxable, in case of a claim under section 18(1)(d).

The details furnished in the declaration above shall be duly certified by a practicing chartered accountant or cost accountant if the total amount of the claim on account of Central tax, State Tax, Union Territory Tax, and Integrated Tax exceeds two lakh rupees as per Rule 40(1)(d).

As per Section 18(2) the registered person shall not be entitled to take the input tax credit in respect of any supply of goods and services or both to him after the expiry of one year from the date of issue of tax invoice relating to such supply.

Example:

Suppose a registered person becomes liable for Registration on 1st June 2021 and has been granted registration, then he can claim credit of inputs lying in stock or inputs in semi-finished or finished goods as on 31st May 2021 provided that the credit relating to invoices of the inputs older than 1 year i.e before 1st June 2020 cannot be claimed as credit.

Moreover as per Rule 40(1)(a) the input tax credit in respect of Capital goods in Case 3 and 4 above shall be claimed after reducing the tax paid on such capital goods by five percentage points per quarter of a year or part thereof from the date of the invoice or such other documents on which the capital goods were received by the taxable person.

Example:

Suppose a registered person ceases to be taxable under Composition Scheme from 1St May 2021 i.e. he is liable to pay tax under section 9 and can also claim credit, so he will be able to claim credit of inputs lying in stock or inputs in semi-finished or finished goods and on capital goods as on 30th April 2021 provided that the credit relating to invoices of the inputs older than 1 year i.e before 1st May 2020 cannot be claimed as credit. Now in this case suppose if the registered person had purchased a capital good having credit of Rs. 50000 each of CGST and SGST with Invoice dated 1St June 2020, then in this case of capital good the amount of credit which can be claimed by the registered person will be as follows:

So total credit that can be claimed for capital good will be:

CGST Credit = Rs. 50000- Rs. 12500(25% of Rs.50000)= Rs. 37500.

SGST Credit = Rs. 50000- Rs. 12500(25% of Rs.50000)= Rs. 37500.

(B) In Case 5 Above:

As per Rule 41(1) in case of sale, merger, de-merger, amalgamation, lease or transfer, or change in ownership of business the registered person shall file Form ITC-02 along with a request for transfer of unutilized input tax credit lying in his electronic credit ledger to the transferee.

Provided that in the case of demerger, the input tax credit shall be apportioned in the ratio of the value of assets of the new units as specified in the demerger scheme (value of assets means the value of the entire assets of the business, whether or not input tax credit has been availed thereon). This formula for apportionment of ITC shall be applicable for all forms of business re-organization that result in the partial transfer of business assets along with liabilities. It’s been clarified that the apportionment formula shall be applied on the ITC balance of the transferor as available in the electronic credit ledger on the date of filing of FORM GST ITC – 02 by the transferor and the ratio of the value of assets should be taken as on the “appointed date of demerger”.

As per rule 41(3) the transferee shall accept such details and on acceptance, the unutilized credit specified in Form GST ITC-02 shall be credited to his electronic ledger.

The transferor shall also submit a copy of a certificate issued by a practicing chartered accountant or cost accountant certifying that the sale, merger, de-merger, amalgamation, lease, or transfer of business has been done with a specific provision for the transfer of liabilities as per rule 41(2).

Example:

A Company ‘X’ in Gujarat has total assets of Rs.250 crore on 01.04.2020. On 01.07.2020 it disposes assets amounting to Rs.50 crores. On 1.10.2020 it demerges a part of its business to Company ‘Y’ and as a result of such demerger it transfers assets of Rs.50 crore to Company ‘Y’. The total assets of Company X on 01.10.2020 i.e. on the date of the demerger was Rs.200 crore.

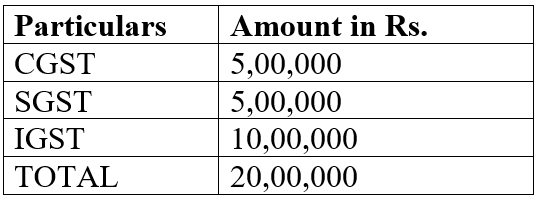

The amount of unutilized credit lying in the credit ledger of Company X at the time of filing Form ITC-02 is as follow:

What will be the amount of unutilized credit which can be transferred by Company X to Company Y on account of Demerger??

Ans: As per rule 41(1) the input tax credit shall be apportioned in the ratio of the value of assets of the new units as specified in the demerger scheme. It’s been clarified by the department that the apportionment formula shall be applied on the ITC balance of the transferor as available in electronic credit ledger on the date of filing of FORM GST ITC – 02 by the transferor and the ratio of the value of assets should be taken as on the “appointed date of demerger”.

Accordingly Ratio will be = 50/200*100 = 25%.

Total credit at time of filing ITC 02 is:

So the amount of credit to be transferred will be

20,00,000*25%= Rs.5,00,000.

It is at the option of the transferor in whatever proportion it wants to transfer credit under each head subject to the ITC balance available under each concerned tax head.

A new rule 41A was also inserted through notification 03/2019 dated 29.01.2019 to allow for the transfer of credit from one business to another business in case of separate registration for multiple places of business within a State or Union Territory by filing the details in Form GST ITC-02A electronically on the common portal.

Conclusion:

The registered person should take care of the above provisions so that the eligible credit can be claimed and does not get lapse, whether at the time of registration or transfer of business.

Disclaimer:

This article is for information purposes only. The information compiled above is based on my understanding and review. Any suggestions to improve the above information are welcome with folded hands, with appreciation in advance. All readers are requested to form their considered views based on their own study before deciding conclusively on the matter. The writer disclaims all liability in respect to actions taken or not taken based on any or all the contents of this article to the fullest extent permitted by law. Do not act or refrain from acting upon this information without seeking professional legal counsel.

Feedbacks are invited at paliwal100991@yahoo.com

Optotax is a Technology Platform Trusted by 50,000+ Tax Professionals across the Country for their 1 Million+ Clients.

Optotax is India’s No. 1 GST Platform and is Exclusively Free for all Tax Professionals.

Our mission is to Empower Tax Professionals and Simplify their practice.

To achieve our mission, we provide a single platform where the Tax Professionals can manage their compliance work in a simplified manner and also gets the opportunity to learn and upgrade knowledge with the help of knowledge-sharing webinars conducted by the best faculties across the country, Taxation related updates, Newsletters, Blogs, Articles, etc.